Meet our CODE_n CONTEST Finalists 2016: fino from Germany

These days, even your bank account switch happens digital and runs off paperless. The next CODE_n finalist in our blog series – fino – offers a digital account switch service. By now, more than 80 banks are using fino’s service, which helps them in the on-boarding process of new customers. We talked to Florian Christ, founder and CEO of fino. In our interview, he tells us all there is to know about his FinTech.

![]() What is fino all about? How did you come up with the idea?

What is fino all about? How did you come up with the idea?

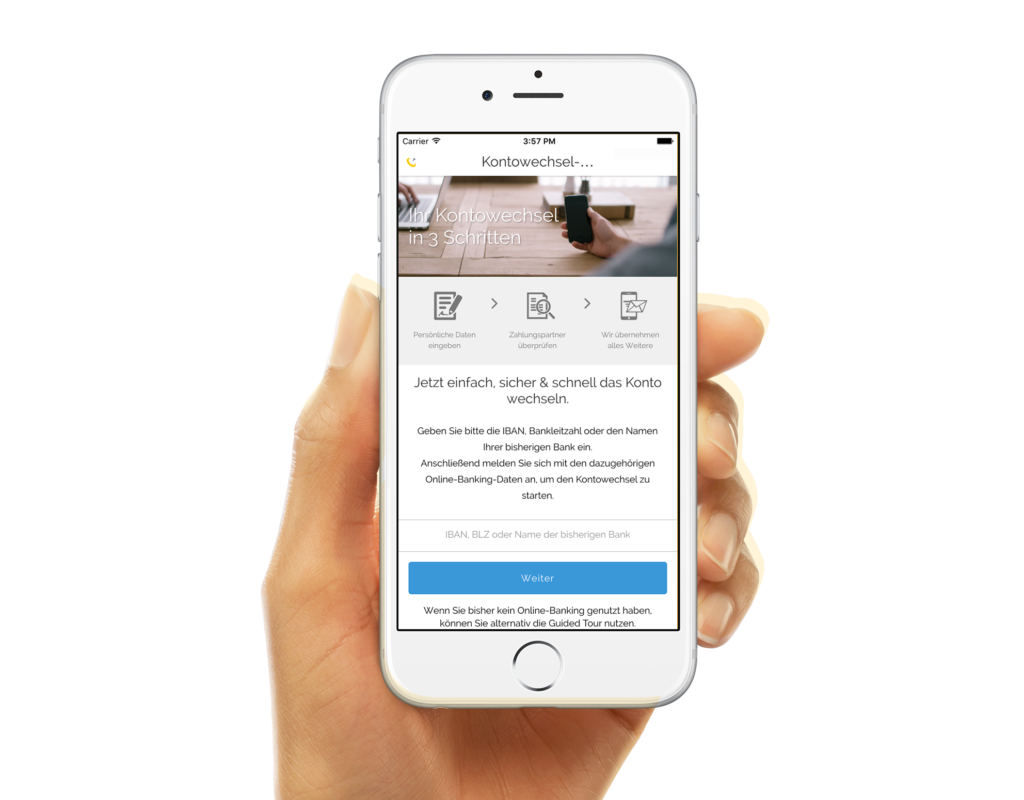

Florian: At the end of 2014, fino started with the idea to enable people switching an existing bank account to a new bank within a few minutes without any paperwork. During that time, an account switch to a new bank was only possible with a lot of paperwork for both the customer and the bank. After building the founding team of fino, the development for the digital account started in May 2015. In September 2015, just six months later, the first version of the digital account switch was ready for launch as a web and mobile solution. Today, two years later, the account switch service has been used by thousands of customers across Germany, helping them to move their old account to a new bank.

Meanwhile, more than 80 banks such as Commerzbank, 1822direkt, Wüstenrot and others are using the digital account switch of fino. The service helps banks in the onboarding process of new customers. Within that context, fino has developed a range of additional digital services in the past six months. All services were developed in close collaboration with banks. This includes a credit card and deposit switch application, as well as new processes for account opening and loan applications.

“Digital Disruption“ – that’s the motto of this year’s CODE_n CONTEST. What makes your solution innovative, what makes it disruptive?

Florian: fino is the pioneer in digital switching services for banks. As the first provider of a digital account switch solution, fino has solved a big problem for banks. The account switch is digital and runs off paperless. The organizational effort for the transfer of direct debit mandates, standing orders and account terminations is minimized considerably. Instead of researching and informing all payment partners such as utilities, telephone service providers or landlords, the fino account switch service takes care of it automatically with a few clicks. Our other switching products, such as the credit card and deposit switch, follow the same principles.

The breakthrough in our product portfolio is the link between the digital services offered to the customer and the established points of contact by bank employees. Our intelligent expenditure account filters the transactions from the account switch and categorizes the data. The data supplied by the intelligent expenditure account allows the bank consultants to get started in intensive consultations quickly.

With the help of a stored set of rules, the revenue from the intelligent expenditure account are classified by an intelligent algorithm. They thus form the basis for our real-time credit rating.

Our contract safe imports all contracts from the category system of the intelligent expenditure account and shows them to the customers in an overview. The foundation for a long-term customer loyalty is created. Similar to the AppStore, our intelligent micro- services can be combined flexible. With the help of our extensive partner- and product database recommendations for the customer can be derived without having to keep the personal information of customers.

You’re one of the 13 finalists in the Applied FinTech contest cluster. Which challenges do you think young companies have to face in this sector? How do you handle these challenges?

Florian: One of the biggest challenges across industries is common to all startups – gain confidence. A young startup is always viewed critically and scrutinized by the seasoned companies. Right from the start we have positioned ourselves as a partner on the side of the banks and not as a competitor. We don’t store customer data and don’t get in touch with the customer. With our promise to the banks “your customer stays your customer” we were able to win the trust quickly and win the first banks as a reference customer in less than six months. For us, data security is the basic requirement. For this reason, we our data security is checked by an independent laboratory.

Staff resources are another challenge for us. Young people feel the financial issues as boring and unattractive because they don’t have many points of contact left with the branch. Now, our team consists of 25 employees who have taken up the cause to revolutionize the banking and pursue their work with passion. We are always looking for motivated colleagues with initiative who would like to continuously extend our role as a pioneer.

Your partners include branch banks as well as direct banks. Do you think one of them will be more present than the other in the financial market in the future?

Florian: From our experience, we can say that both types of banks are justified. fino started with the account switch as a self-service. Customers can switch their account within eight minutes comfortably from their home. Today, after thousands of account switches, we can see that about 40 % of customers switch their account after 6 pm at home from their couch. Nevertheless, another finding is that the branch business is the driving force, because many customers like to use the fino account switching service in the store with their bank manager.

Thanks so much for the interview, Florian!

Write a comment